Also question is, are trusts subject to estate tax?

Although a revocable trust may help avoid probate, it is usually still subject to estate taxes. Also, since the assets have been transferred to the trust, you are relieved of the tax liability on the income generated by the trust assets (although distributions will typically have income tax consequences).

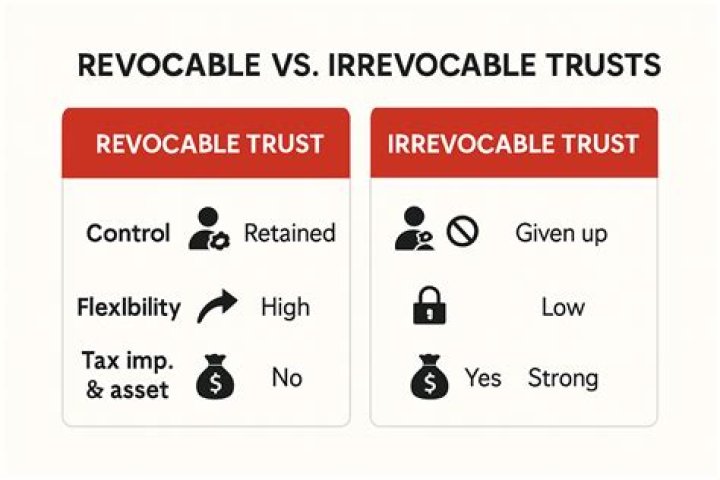

Likewise, are revocable trusts included in gross estate? These assets are included in the gross estate. To form a trust, the grantor must transfer his ownership in the trust property to the trustee. However, since the decedent retains the ability to regain the assets in a revocable trust, the property he donated to the trust is included in his estate.

One may also ask, how is a revocable trust taxed after death?

The Revocable Trust tax implications, following the death of the Grantor, impact both the Grantor's Estate and the Beneficiaries'. However, any income earned by the Trust assets or principal after the date of the Grantor's death is reported in a separate tax return for the Trust.

Are revocable trusts subject to probate?

The primary advantage of a revocable trust is to avoid probate. Another advantage to having a revocable trust is during the lifetime of the grantor if they become disabled, then the trustee, the successor trustee, would come in and manage those assets on behalf of the grantor.

Related Question Answers

How much can you inherit without paying taxes in 2020?

In 2020, there is an estate tax exemption of $11.58 million, meaning you don't pay estate tax unless your estate is worth more than $11.58 million. (The exemption is $11.7 million for 2021.) Even then, you're only taxed for the portion that exceeds the exemption.Does the IRS know when you inherit money?

Money or property received from an inheritance is typically not reported to the Internal Revenue Service, but a large inheritance might raise a red flag in some cases. When the IRS suspects that your financial documents do not match the claims made on your taxes, it might impose an audit.What happens when you inherit money from a trust?

If you inherit from a simple trust, you must report and pay taxes on the money. By definition, anything you receive from a simple trust is income earned by it during that tax year. Any portion of the money that derives from the trust's capital gains is capital income, and this is taxable to the trust.Do beneficiaries pay taxes on trust distributions?

Beneficiaries of a trust typically pay taxes on the distributions they receive from the trust's income, rather than the trust itself paying the tax. However, such beneficiaries are not subject to taxes on distributions from the trust's principal.Can I put my house in trust to avoid inheritance tax?

A trust can be a good way to cut the tax to be paid on your inheritance. But you need professional advice to get it right. This means that when you die their value normally won't be counted when your Inheritance Tax bill is worked out. Instead, the cash, investments or property belong to the trust.How can I avoid US estate tax?

10 Ways to Reduce or Avoid Estate Taxes- 10 Ways to Avoid or Minimize the Federal Estate Tax.

- Buy Life Insurance Now and Use the Benefit to Pay the Tax.

- Move to a State without Estate Taxes.

- Gift Assets While you are Alive.

- Set up an Irrevocable Life Insurance Trust.

- Set up a Charitable Trust.

- Set up a Donor Advised Fund.

Who pays the taxes on a revocable trust?

Revocable trusts are the simplest of all trust arrangements from an income tax standpoint. Any income generated by a revocable trust is taxable to the trust's creator (who is often also referred to as a settlor, trustor, or grantor) during the trust creator's lifetime.Should I put my house in a revocable trust?

Should you put your house in a revocable trust or irrevocable trust? Putting your house in a revocable trust still allows you to change the terms of the trust or remove the house from the trust if you want to. Taxes and personal finances are generally easier to manage with a revocable trust.What happens to revocable trust upon death?

When the maker of a revocable trust, also known as the grantor or settlor, dies, the assets become property of the trust. If the grantor acted as trustee while he was alive, the named co-trustee or successor trustee will take over upon the grantor's death.What should you not put in a revocable trust?

Assets that should not be used to fund your living trust include:- Qualified retirement accounts – 401ks, IRAs, 403(b)s, qualified annuities.

- Health saving accounts (HSAs)

- Medical saving accounts (MSAs)

- Uniform Transfers to Minors (UTMAs)

- Uniform Gifts to Minors (UGMAs)

- Life insurance.

- Motor vehicles.

Do revocable living trusts file tax returns?

The income from the revocable (living) trust is to be reported on the personal income tax returns of the Trustors (persons who formed the trust). The IRS and California taxing authorities do not recognize a living (revocable) trust as a separate taxpaying entity as long as both Trustors are alive.How do trusts avoid taxes?

They give up ownership of the property funded into it, so these assets aren't included in the estate for estate tax purposes when the trustmaker dies. Irrevocable trusts file their own tax returns, and they're not subject to estate taxes, because the trust itself is designed to live on after the trustmaker dies.Do you have to report inheritance money to IRS?

Inheritances are not considered income for federal tax purposes, whether you inherit cash, investments or property. However, any subsequent earnings on the inherited assets are taxable, unless it comes from a tax-free source.What is the federal income tax rate for trusts?

For the 2020 tax year, a simple or complex trust's income is taxed at bracket rates of 10%, 24%, 35%, and 37%, with income exceeding $12,950 taxed at that 37% rate.Do beneficiaries have to pay taxes on inheritance?

Generally speaking, inheritance is not subject to tax in California. If you are a beneficiary, you will not have to pay tax on your inheritance. There are a few exceptions, such as the Federal estate tax.Are trusts considered part of an estate?

Upon the grantor's death, the assets in the trust are generally not considered part of his or her estate and are therefore not subject to estate taxes.What are the tax advantages of a revocable trust?

A Revocable Trust does not reduce income taxes, estate taxes, gift taxes, generation skipping taxes or inheritance taxes. In short, Living Trusts provide no tax advantages. If someone is trying to sell you on the idea of forming a Revocable Trust based on tax savings, run away!How does a trust work after someone dies?

How Do You Settle A Trust? The successor trustee is charged with settling a trust, which usually means bringing it to termination. Once the trustor dies, the successor trustee takes over, looks at all of the assets in the trust, and begins distributing them in accordance with the trust. No court action is required.Who owns the property in a revocable trust?

grantor trustCan a trustee remove a beneficiary from a trust?

In most cases, a trustee cannot remove a beneficiary from a trust. This power of appointment generally is intended to allow the surviving spouse to make changes to the trust for their own benefit, or the benefit of their children and heirs.Does a revocable trust protect assets from nursing home?

A revocable living trust will not protect your assets from a nursing home. This is because the assets in a revocable trust are still under the control of the owner. To shield your assets from the spend-down before you qualify for Medicaid, you will need to create an irrevocable trust.Why is it good to avoid probate?

The two main reasons to avoid probate are the time and money it can take to complete. Remember that probate is a court process, and along with the various proceedings and hearings, simply gathering assets and paying off debts of an estate can take months or even years.What you should never put in your will?

Types of Property You Can't Include When Making a Will- Property in a living trust. One of the ways to avoid probate is to set up a living trust.

- Retirement plan proceeds, including money from a pension, IRA, or 401(k)

- Stocks and bonds held in beneficiary.

- Proceeds from a payable-on-death bank account.