Also question is, what are the assumptions used in CAPM and arbitrage pricing theory?

Three Underlying Assumptions of APT

The theory does, however, follow three underlying assumptions: Asset returns are explained by systematic factors. Investors can build a portfolio of assets where specific risk is eliminated through diversification. No arbitrage opportunity exists among well-diversified portfolios.

One may also ask, what are the principles of arbitrage pricing theory? Arbitrage pricing theory (APT) is a multi-factor asset pricing model based on the idea that an asset's returns can be predicted using the linear relationship between the asset's expected return and a number of macroeconomic variables that capture systematic risk.

Just so, what are the assumptions of CAPM?

The CAPM is based on the assumption that all investors have identical time horizon. The core of this assumption is that investors buy all the assets in their portfolios at one point of time and sell them at some undefined but common point in future.

What are the assumptions of CAPM and are they reasonable?

The CAPM makes assumptions about investor preferences (more return is preferred to less, and risk must be rewarded), about investors' behaviour (risk is variance of the portfolio, and mean and variance of returns are the normal investor's key considerations) and about the world (investor's forecasts are homogeneous and

Related Question Answers

What are the basic assumptions of arbitrage pricing theory apt?

Major assumptions of Arbitrage Pricing Theory (APT) are (1) returns can be described by a factor model, (2) there are no arbitrage opportunities, (3) there are a large number of securities so it is possible to form portfolios that diversify the fi rm-specifi c risk of individual stocks and (4) the financial markets areWhich of the following is not an assumption of CAPM?

The correct answer is option "c" and that is not an assumption of CAPM model. The investor is limited by his wealth and price of asset only.Are CAPM assumptions realistic?

The CAPM has serious limitations in real world, as most of the assumptions, are unrealistic. Many investors do not diversify in a planned manner. Besides, Beta coefficient is unstable, varying from period to period depending upon the method of compilation. They may not be reflective of the true risk involved.How is CAPM used?

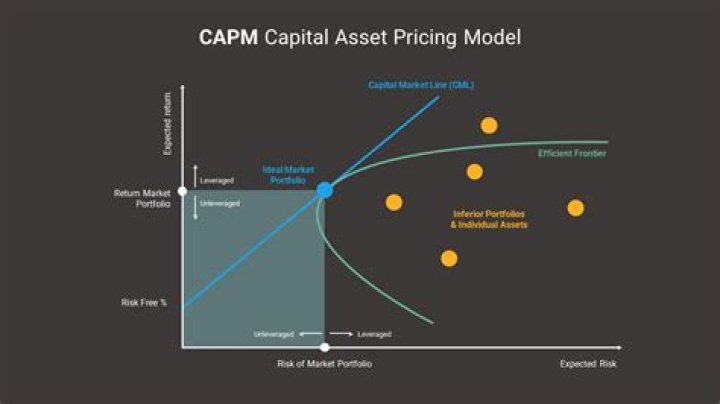

The Capital Asset Pricing Model (CAPM) describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is widely used throughout finance for pricing risky securities and generating expected returns for assets given the risk of those assets and cost of capital.What is Ri in CAPM?

The formula used in CAPM is: E(ri) = rf + βi * (E(rM) - rf), where rf is the risk-free rate of return, βi is the asset's or portfolio's beta in relation to a benchmark index, E(rM) is the expected benchmark index's returns over a specified period, and E(ri) is the theoretical appropriate rate that an asset shouldWhich of the following is an assumption of the APT?

The primary assumption of the APT is that security returns are generated by a linear factor model. In practice, researchers claim that we need at least two factors for the APT model. The APT does not assume that investors make decisions according to the mean-variance rule.How is the CAPM considered a special case of arbitrage pricing theory?

In some ways, the CAPM can be considered a "special case" of the APT in that the securities market line represents a single-factor model of the asset price, where beta is exposed to changes in value of the market. A disadvantage of APT is that the selection and the number of factors to use in the model is ambiguous.What are the principles of arbitrage?

Arbitrage means taking advantage of price differences in different markets. In well-functioning markets, arbitrage opportunities are quickly exploited, and the resulting increased buying of underpriced assets and increased selling of overpriced assets return prices to equivalence. Assume the risk-free rate is 5%.Why is arbitrage pricing theory better than CAPM?

APT concentrates more on risk factors instead of assets. This gives it an advantage over CAPM simply because you do not have to create a similar portfolio for risk assessment. While CAPM assumes that assets have a straightforward relationship, APT assumes a linear connection between risk factors.In what conditions would CAPM be equal to APT?

If the market risk is used as the only factor, the APT would equal CAPM.What model would you choose between CAPM and APT?

The arbitrage pricing theory is an alternative to the CAPM that uses fewer assumptions and can be harder to implement than the CAPM. While both are useful, many investors prefer to use the CAPM, a one-factor model, over APT, which requires users to quantify multiple factors.What is CAPM and APT?

The capital asset pricing model (CAPM) provides a formula that calculates the expected return on a security based on its level of risk. Arbitrage pricing theory (APT) is a well-known method of estimating the price of an asset.How do you determine if there is an arbitrage opportunity?

Arbitrage opportunities exist when an investor either invests nothing and yet still expects a positive payoff in the future or receives an initial net inflow on an investment and still expects a positive or zero payoff in the future.Which of the following is the major difference between the Capital Asset Pricing Model CAPM and arbitrage pricing theory apt?

arbitrage pricing theory (APT)? (A) CAPM uses a single systematic risk factor to explain an asset's return whereas APT uses multiple systematic factors. Under CAPM, the beta coefficient of the risk-free rate of return is assumed to be higher than that of any. asset in the portfolio.How are apartments used in investment decisions?

The APT offers analysts and investors a multi-factor pricing model for securities, based on the relationship between a financial asset's expected return and its risks. The APT aims to pinpoint the fair market price of a security that may be temporarily incorrectly priced.Why is CAPM flawed?

Research shows that the CAPM calculation is a misleading determination of potential rate of return, despite widespread use. The underlying assumptions of the CAPM are unrealistic in nature, and have little relation to the actual investing world.Why is the assumption of homogeneous expectations critical for the CAPM?

The homogeneous expectations assumption argues that investors will choose an investment plan that guarantees the highest profit from many plans with different returns at a given risk. Investors will select a plan bearing the lowest risk in the same vein if presented with plans with different risks.How do you determine if a stock is undervalued or overvalued using CAPM?

Beta is an input into the CAPM and measures the volatility of a security relative to the overall market. SML is a graphical depiction of the CAPM and plots risks relative to expected returns. A security plotted above the security market line is considered undervalued and one that is below SML is overvalued.How would you interpret an assumption of CAPM All investments are infinitely divisible?

All investments are infinitely divisible, which means that it is possible to buy or sell fractional shares of any asset or portfolio.Which of the following does the Capital Asset Pricing Model CAPM assume?

The Capital Asset Pricing Model (CAPM) is the product of a financial investment theory that reflects the relationship between risk and expected return. The model assumes a linear relationship.How do you use CAPM to value stock?

How is CAPM calculated? To calculate the value of a stock using CAPM, multiply the volatility, known as “beta,†by the additional compensation for incurring risk, known as the “Market Risk Premium,†then add the risk-free rate to that value.What limitations are associated with the use of beta for asset pricing?

Disadvantages of BetaBeta is useful in determining a security's short-term risk, and for analyzing volatility to arrive at equity costs when using the CAPM. However, since beta is calculated using historical data points, it becomes less meaningful for investors looking to predict a stock's future movements.