Similarly one may ask, what is trial balance describe various methods of preparing trial balance and its important functions?

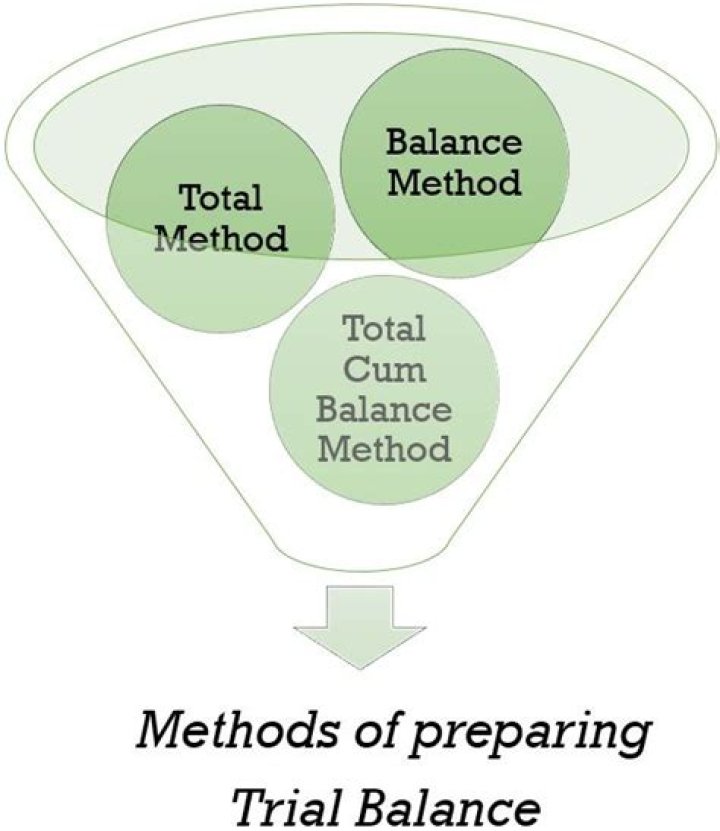

Total Method or Gross Trial Balance:

If any particular account has a total on one side, it will be entered either in the debit column or the credit column as the case may be. It promotes the arithmetical accuracy of the accounts. Extraction of ledger balances is not required at the time of preparation of Trial Balance.

Beside above, what are the various method of preparation of trial balance? Top 2 Methods of Preparing Trial Balance (With Specimen)

- Total Method: In this method, ledger accounts are not balanced. They are totaled.

- Balance Method: Under this method, the closing balances of ledger accounts are tabulated in a separate statement. The brought down balances are brought to this statement.

Moreover, what is trial balance and functions of trial balance?

Trial Balance is a statement showing all the ledger account balances whether debit or credit on a particular date. A firm prepares the trial balance to check the arithmetical accuracy of the accounts. A trial balance is a summary of all the ledger accounts.

What is trial balance how a trial balance is prepared explain?

The trial balance is prepared after posting all financial transactions to the journals and summarizing them on the ledger statements. The trial balance is made to ensure that the debits equal the credits in the chart of accounts. Add up the amounts of the debit column and the credit column.

Related Question Answers

What are the objectives of trial balance?

The purpose of a trial balance is to ensure that all entries made into an organization's general ledger are properly balanced. A trial balance lists the ending balance in each general ledger account. The total dollar amount of the debits and credits in each accounting entry are supposed to match.What are the three types of trial balances?

There are three types of trial balances: the unadjusted trial balance, the adjusted trial balance and the post- closing trial balance. All three have exactly the same format. The unadjusted trial balance is prepared before adjusting journal entries are completed.Which of the following is the most popular method of preparing a trial balance?

Which one of the following is the most popular method of preparing a trial balance: Balance method.What are the two types of trial balance?

There are two other types of trial balance: the adjusted trial balance which is prepared after adjusting entries are prepared and posted, and the post-closing trial balance which is prepared after closing entries. These two are prepared in later steps of the accounting process.What are the difference between trial balance and balance sheet?

The main difference between the trial balance and a balance sheet is that the trial balance lists the ending balance for every account, while the balance sheet may aggregate many ending account balances into each line item. The balance sheet is part of the core group of financial statements.What are key features of a trial balance?

In Trial balance, all the ledger balances are posted either on the debit side or credit side of the statement. The total of debit balance in trial balance should match with a total of credit balance, only then it is said to be arithmetically accurate.What are the rules of trial balance?

RULES OF TRIAL BALANCE- All assets must be put on the debit side.

- All liabilities must be put on the credit side.

- All income or gain must be recorded on the credit side.

- All expenses must be recorded on the debit side.

What are the key features of a balance sheet?

Key Points A standard company balance sheet has three parts: assets, liabilities and ownership equity.What are the main objectives of accounting?

The following are the main objectives of accounting:- To maintain full and systematic records of business transactions: ADVERTISEMENTS:

- To ascertain profit or loss of the business: Business is run to earn profits.

- To depict financial position of the business:

- To provide accounting information to the interested parties: